Banks are not only reserving the money you deposit but also loan money out. Where do banks get funds for loans? They may use the same money you deposit to give them someone else and vice versa. The system in which banks don’t hold 100% of all deposited money but rather a small fraction of them is called “fractional reserve banking.”

This article explains what fractional reserve banking is, how it works, what are the pros and cons of this system, and how it is different from other types of banking.

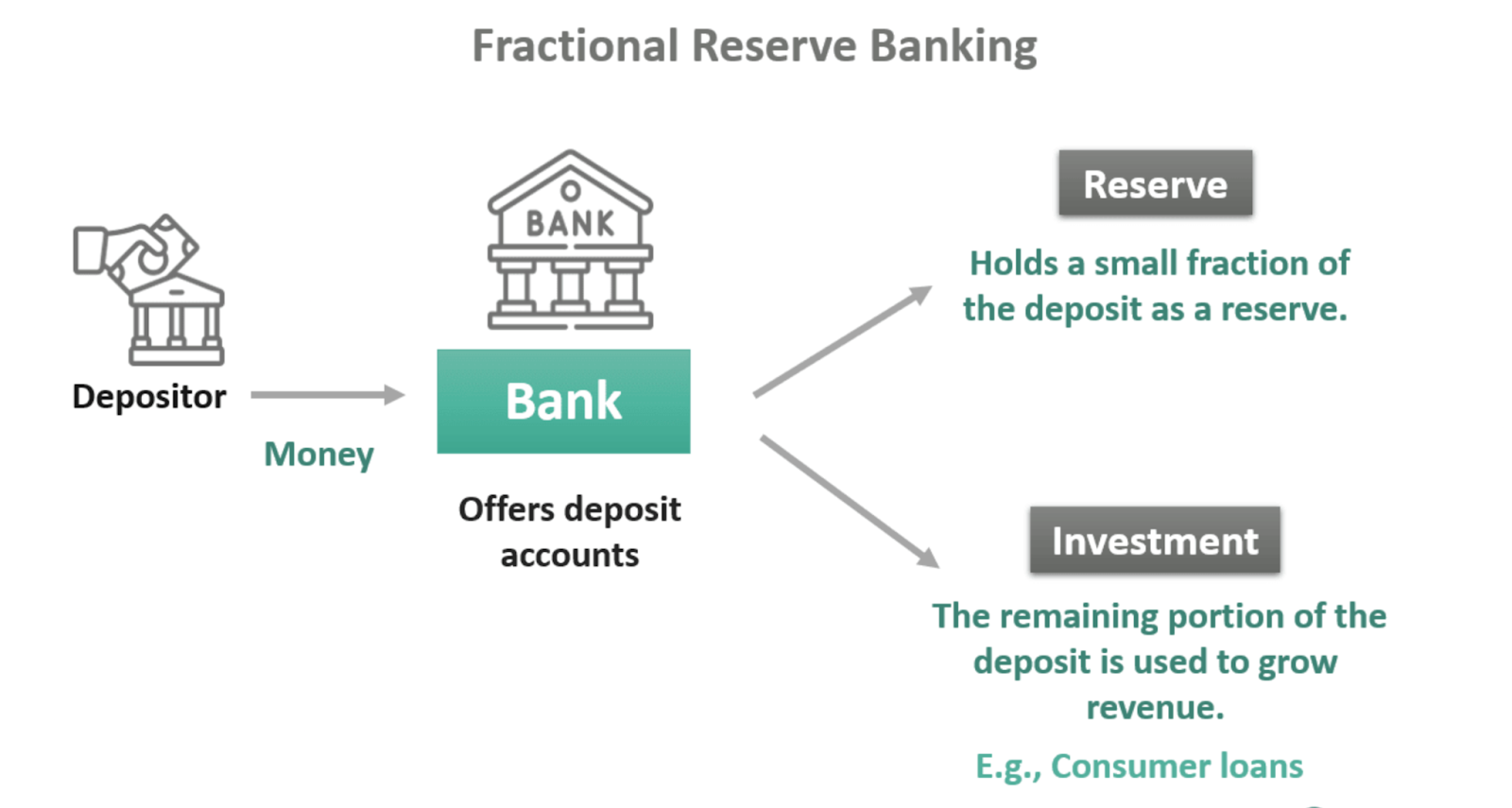

What Is Fractional Reserve Banking?

Fractional reserve banking is a banking system that doesn’t hold all the users’ assets all the time. Instead, banks hold only a fraction of the deposited money and use the rest of funds for giving loans. If a client requests withdrawing much money, this money can be taken from the other clients’ deposits.

The purpose of fractional reserve banking is expanding the economy. It is achieved via spreading free capital through lending. At no cost more people receive money and the ability to invest and spend them. Nowadays, the fractional reserve banking system is pretty much mainstream.

Image source: Wall Street Mojo

In most countries, banks are obliged to hold a certain minimum amount of money on their balance sheets. This measure is supposed to prevent collapse in the event if too many clients request withdrawals simultaneously. However, not everywhere banks must follow this rule. In 2020, the Federal Reserve of the US freed banks from the obligation of keeping any certain amount of clients’ money on the balance sheets. Instead, it offered an incentive—banks earn interest on the reserve funds they hold.

How Does It Work?

If you are going to interact with the bank, you should sign a contract. Most probably, one of the sections of this contract states that the bank is allowed to use a certain share of your deposits for loaning out to other clients. It won’t hinder your ability to withdraw all your money at any moment. In the event if you are going to withdraw more than this share, the bank will add some money from the other client’s deposit as the bank never keeps the entire sum of your deposit reserved at any given moment.

Banks even use the money you deposit to savings accounts. A certain amount can be used by banks for loans. You will be paid for the use of your money.

If banks run short of money to cover the debts, fund withdrawals or loans, they can borrow money from each other. Alternatively, banks can get loans from the Federal Reserve at a higher interest rate which makes it more beneficial to seek support from the other banks, not from the Federal Reserve.

Example

The example below illustrates how fractional reserve banking works. You deposit $4,000 in a savings account. Let’s say, the interest paid by the bank is 1%. You get the interest and the bank gets the money that can be used for lending as it can access most of your deposit’s amount. The interest paid for the money you keep in the bank is a stimulus to not move them from the account.

The 90% of the $4,000 you deposited on the savings account is used by the bank for loaning out other customers. Think of money from the other deposits and you will see that several clients that deposit money on the savings accounts, release over $10,000 for the use to other people.

At the same time, the balance on your account is still $4,000. Let’s assume, there are four clients that have $4,000 on their accounts and receive a 1% as an annual interest. The bank can use $14,400 (90%) of these $16,000 for loans. If someone needs a loan of $1,600, the bank may use 10% of the money deposited by these four clients and provide a $1,600 loan to a fifth customer at 5% per year. The bank created money and earned something to cover your interest.

Fractional Reserve Banking vs. Other Types of Banking

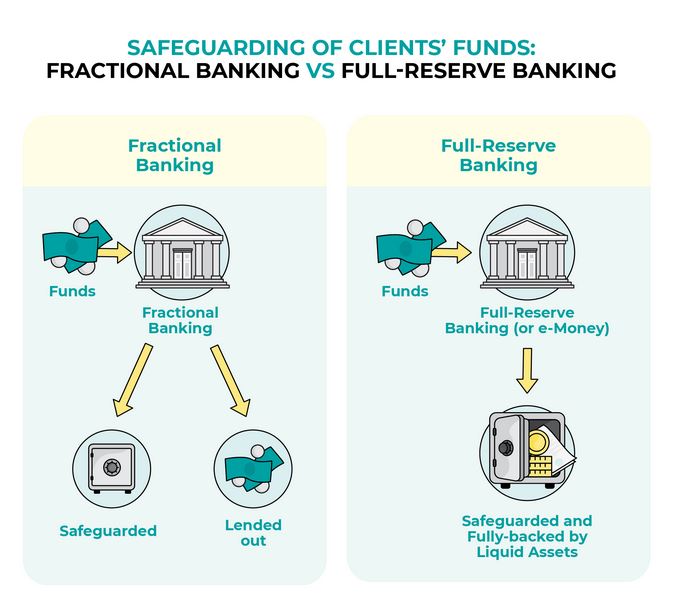

In the modern-day era, fractional reserve banking is used in most countries as keeping 100% of clients’ money as a reserve is not practical. The system in which banks hold the clients’ deposits in their entirety all the time sets the money devaluing process as it is the only way to profit from holding this money. This method requires holding large amounts to get free capital that can be used for lending. Such conditions are slowing the economic development speed down.

Image source: Civils Daily

Another system is backing the money by gold or other precious metals and commodities. This system puts a limit on the economic potential as each country has only a limited amount of gold and can’t increase it quickly if needed. Fractional reserve banking allows increasing the capital supply in the country in accord with the demand for it.

Pros & Cons

Now, let’s take a look at the pros and cons of fractional reserve banking.

Pros

Banks don’t have to hold much money: Banks are using the money deposited by the clients without taking this money away from them. This money is getting injected into economic growth. The banks make this money work.

Lending stimulates the economy: Without free capital the economy won’t grow. People want to save their money but banks let this money work instead of keeping them still. This money is used by other companies or individuals. Many of the loan types wouldn’t have existed without fractional reserve banking.

This system can be controlled: Central banks control the situation through changing the rules for the percentage of the reserve that banks must keep on their balance sheets. The less money is required to keep, the more money banks can use for lending. This regulation tool is frequently used in China.

Cons

Banks can face difficulties in returning people their money while facing a bank run: History knows the precedents when masses of people scared by some unfavorable events (like COVID panic) may want to withdraw all their money from their accounts. Fractional reserve system is not capable of returning most of the people’s deposits back to the clients.

The lending surge may worsen the overheating economy: The economic growth is associated with consumers spending money more eagerly and in larger amounts while banks are loaning out more. When new money is made via lending, the demand rises making the prices higher. The production of goods increases to satisfy the growing demand. In such circumstances, the economy may overheat quickly.

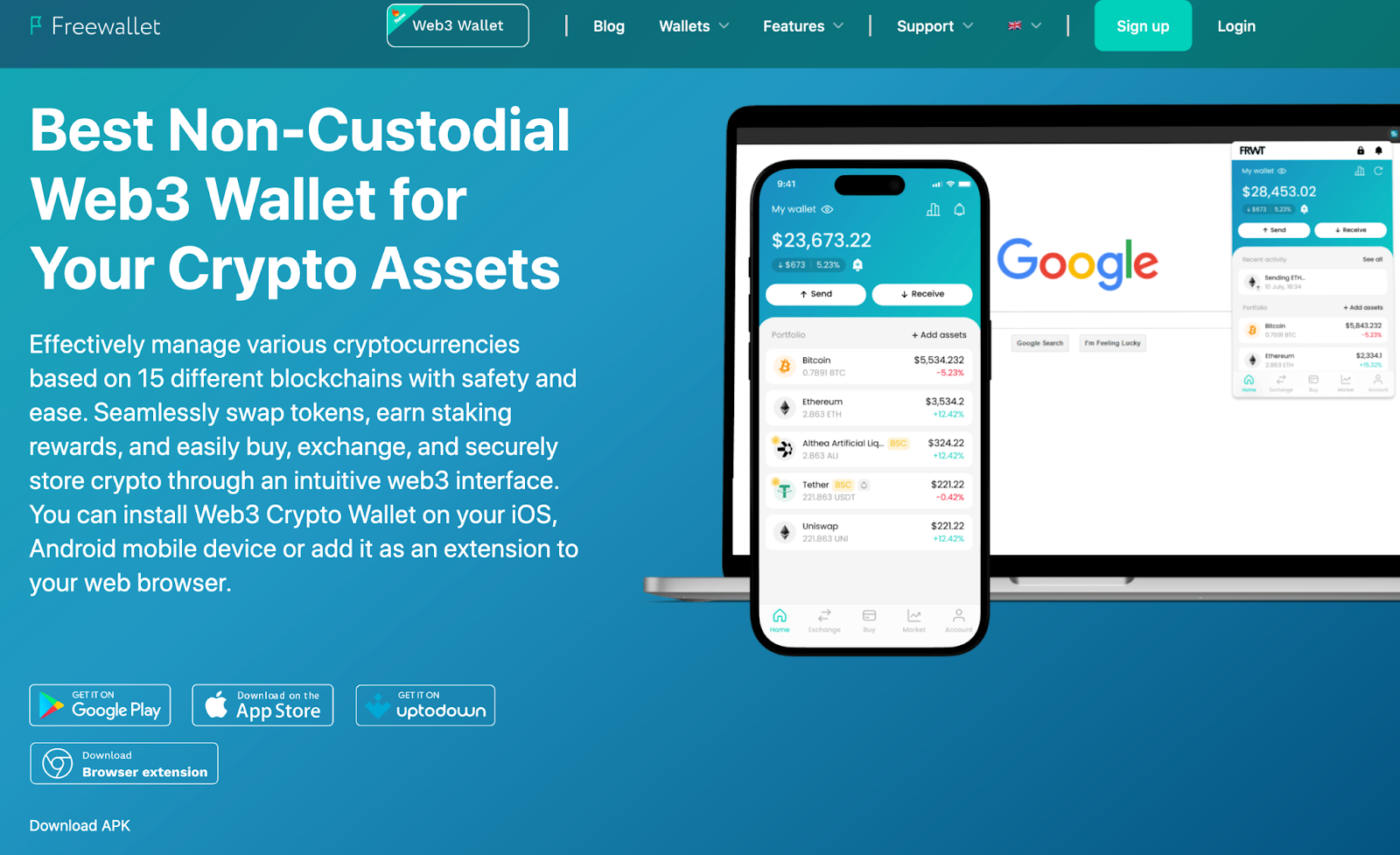

Freewallet Web3 Wallet

To decrease your dependence on banks while keeping the ability of growing wealth and spending money online, you may opt to use a multifunctional non-custody web3 crypto wallet from Freewallet.

The web3 wallet was released in February 2024 as a mobile app and a browser extension. It supports over 1,000 cryptocurrencies based on 15 blockchains. You can use even more assets if you connect a custom blockchain. The wallet allows users to buy crypto by card via the partnership with local payment operators.

You can instantly swap crypto tokens within the wallet interface or exchange them via in-built centralized and decentralized crypto exchanges.

The security of your funds is guaranteed. The wallet is non-custodial, meaning that no one but you has access to your private keys. You can always access your coins using a seed phrase. The account can be protected via the PIN or a passcode. Optionally, you can turn on biometric signin and spending limits.

To get the best from the DeFi sector using Freewallet web3 wallet you can join the yield farming and staking platforms and other dApps via WalletConnect.

Conclusion

Economy is trickier than it may seem on the surface. Through fractional reserve banking you can see that such a system that uses most of the clients’ deposits instead of keeping them prepared for withdrawals brings more benefits than problems. However, the system is far from being perfect, so you should understand well the costs of its advantages.

Related

Stay tuned

Subscribe for weekly updates from our blog. Promise you will not get emails any more often.

Our authors

Most Popular

New Posts

Stay tuned

Subscribe for weekly updates from our blog. Promise you will not get emails any more often.

Our authors